1. Standardised international account planning

1.1 Bases

1.1.1 Targets of standardised processes

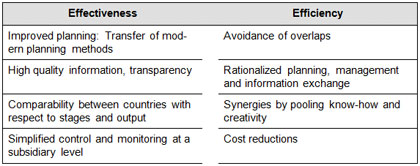

Standard processes are not only the prerequisite for standardised international positioning, but also disclose a variety of approaches in order to realise competitive advantages in terms of higher efficiency and effectiveness (Kreutzer 1987, p168).

Table 1: The benefits of standard processes in international advertising planning (Sources: Berndt et al. 2003, p167; Kreutzer 1989, p525).

By centralising planning and creation of advertisement as well as market research savings can be made. Costs can be cut by assigning only one single agency with the conception instead of entrusting local agencies in each country with the same task. Furthermore, cost benefits result from rebates, which are granted for international bookings of certain media, such as a bundle of magazines (Stelzer 1994, p155).

Moreover, standard processes may improve planning as efficient methods can be applied internationally. Account planning can also be delegated to a specialist (Kreutzer 1986, p27 ff.).

Due to given, long-term planning scopes, standard processes may finally contribute to a stronger strategic orientation of the advertisement of foreign subsidiaries and thus sustainably account for a positioning (Kreutzer 1986, p31). This is still quite seldom because national sales companies (NSC) are generally organised in profit centres and measured according to sales objectives. They therefore favour price-oriented advertising with a short-term effect.

1.1.2 Conditions for standard processes

Processes for solving tasks can be standardised as long as they fulfil three criteria

(Landwehr 1988, p58):

- The task has to be repetitive, as the definition of a standard procedure does only make sense,

if it causes rationalisation with repeated tasks. - The information necessary to solve the task has to be ascertainable in order to assess the

pertinence of a standard procedure for similar tasks. - The results have to be observable, i.e. certain moments at which the extent of the target

achievement can be controlled have to be given in order to adapt the progression or extent

of certain procedures in terms of a control loop.

The tasks of international account planning described as follows are considering these three criteria in order to determine the ability of processes to be standardised. Moreover, possibilities for division of work between the manufacturer and the national sales companies are discussed, as account planning is only efficient, if centralised know-how on the one hand and local market knowledge on the other hand are used.

Further Chapters

- Standardised international account planning

- International analysis of the initial situation

- International advertising strategy

- International advertising budget planning

- International planning of advertising design

- International media planning

- International advertising control

- The implementation of international